Buying a Home with a VA Assumable Loan: What Military Buyers Need to Know

If you’ve been looking at homes lately, you’ve probably seen listings advertising an “assumable VA loan.”

With interest rates higher than they were just a few years ago, it’s easy to understand why these homes are getting so much attention.

I’ve had several military buyers ask me recently:

“Should we be looking specifically for assumable loans?”

The answer is…

Maybe.

A VA assumable loan can be an incredible opportunity in the right situation, but it’s important to understand how they work before making them the center of your home search.

What Is a VA Assumable Loan?

A VA assumable loan allows a qualified buyer to take over the seller’s existing mortgage instead of obtaining a brand-new loan.

That means if the seller locked in a low interest rate a few years ago, the buyer may be able to assume that same rate.

For example, instead of financing a home at today’s interest rates, you may be able to take over a loan with a rate of 2.5% or 3%.

That’s a significant difference in monthly payment and one of the reasons assumable loans have become such a popular topic.

Why Buyers Are Interested Right Now

A lower interest rate is the biggest reason assumable loans have become so popular – but it’s not the only benefit.

Depending on the seller’s loan, you may also be assuming a mortgage that’s already several years into its repayment.

That can provide advantages like:

- A lower monthly payment because of the reduced interest rate.

- Fewer years remaining on the loan. For example, if the seller has already made five years of payments on a 30-year mortgage, you may only have about 25 years left to repay.

- Building equity faster. As a mortgage ages, a larger portion of each monthly payment is applied to the principal balance instead of interest.

- Paying off your home sooner than you would with a brand-new 30-year mortgage.

For many buyers, these benefits can make a meaningful difference in both their monthly budget and their long-term financial goals.

However, there are a few important realities every buyer should understand before deciding whether an assumable loan is the right fit.

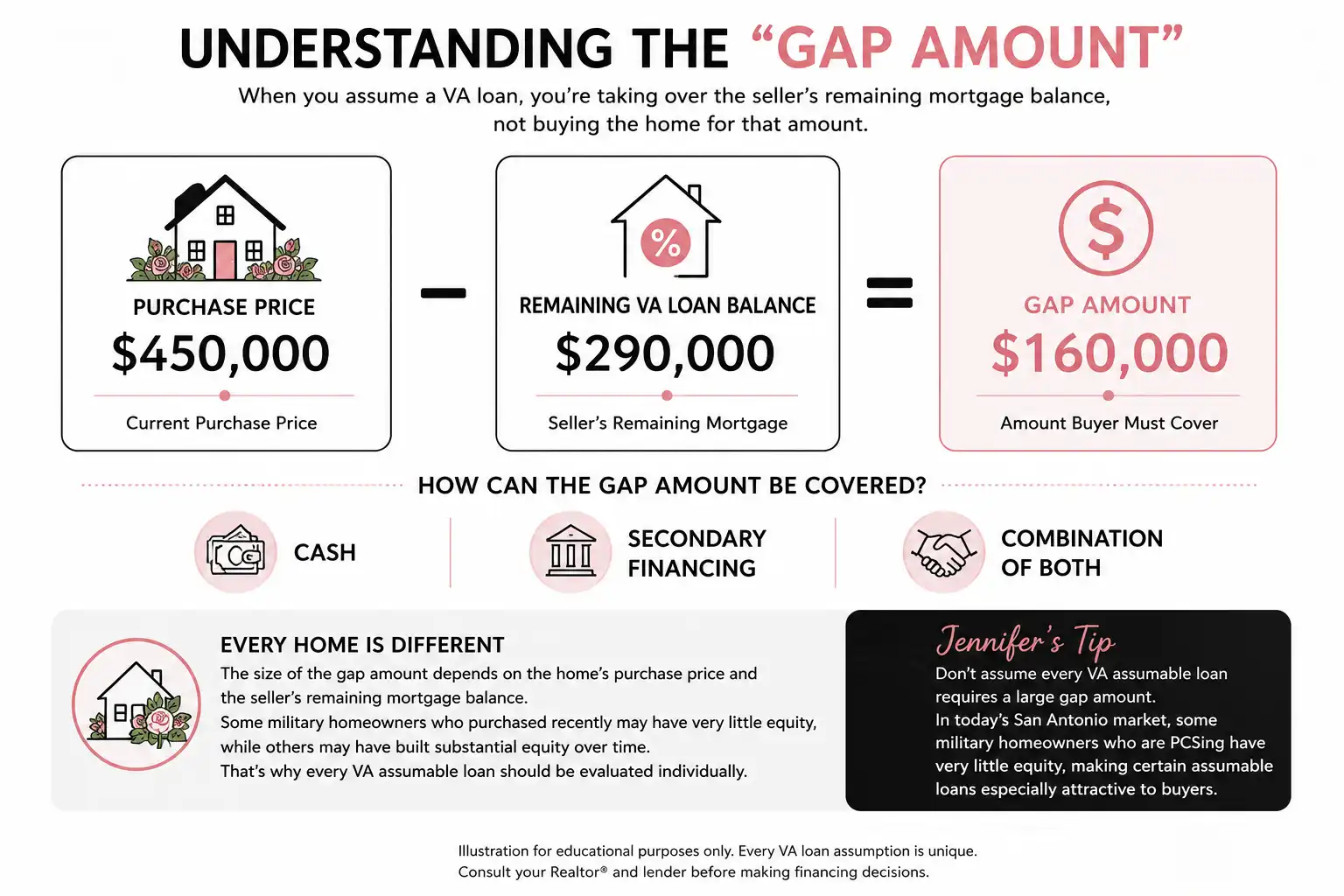

The Biggest Misconception: Understanding the “Gap Amount”

One of the biggest misconceptions about VA assumptions is that assuming a low-interest-rate mortgage means you can buy the home with very little money out of pocket.

In reality, you’re assuming the seller’s remaining loan balance, not purchasing the home for that amount.

If the home’s purchase price is higher than what the seller still owes, the buyer is responsible for covering the difference, often referred to as the “gap amount.” Depending on the situation, that could be be paid with cash, secondary financing, or another approved funding source.

Here’s a simple example of how the gap amount is calculated:

One thing I always remind buyers is that every assumption is different.

In today’s San Antonio market, where home values have remained relatively stable over the past few years, some sellers have built significant equity while others – especially military homeowners who purchased more recently and are now PCSing – may have very little.

That means one assumable loan may require a substantial amount of cash at closing, while another may have a much smaller gap amount. That’s one of the reasons I evaluate assumable loans on a property-by-property basis rather than making assumptions based on the advertised interest rate alone.

It’s also worth remembering that because you’re assuming a loan with fewer years remaining, you’ll typically be paying the loan back over a shorter period than you would with a brand-new 30-year mortgage. That means more of your monthly payment goes toward building equity and less goes toward interest.

While the shorter repayment timeline can increase the principal portion of your monthly payment, the lower interest rate often offsets much, or all, of that difference. Every situation is different, which is why it’s important to compare the complete financial picture before deciding whether an assumable loan is the right fit.

What I Tell My Buyers

When buyers ask me whether they should pursue a VA assumable loan, I get excited because they can absolutely be a fantastic opportunity.

But before we start touring assumable homes, I always make sure we talk through the assumption process itself.

Unlike a traditional mortgage where your lender is driving much of the process, a VA loan assumption requires regular communication between the buyer, the seller, and the mortgage servicer.

There are documents to submit, requests for additional information, and follow-up conversations throughout the process. As your Realtor, one of my jobs is helping keep everyone organized, checking in regularly, and making sure the assumption continues moving forward.

Even with that support, successful assumptions rely on both the buyer and seller staying engaged and responding promptly when the mortgage servicer requests information.

Buyers should also expect the process to take longer than a traditional mortgage. While every mortgage servicer is different, VA loan assumptions generally require more time and coordination than a conventional purchase.

If you’re under a tight deadline – such as a PCS with a firm report date – we’ll want to discuss that early so we can determine whether pursuing an assumption is the right strategy for your situation.

In my experience, understanding the timeline upfront helps everyone set realistic expectations and reduces frustration throughout the transaction.

When a VA Assumable Loan Makes Sense

There are situations where assuming a VA loan can be an excellent strategy.

For example:

- You have substantial savings available.

- You’re receiving proceeds from the sale of another home.

- The seller has relatively little equity.

- The interest rate difference creates significant monthly savings.

- You plan to own the home for many years.

In these situations, assuming a low-interest-rate mortgage may save you a considerable amount of money over time.

When It May Not Be the Best Option

A VA assumption isn’t always the right answer.

It may not make sense if:

- You don’t have enough cash to cover the seller’s equity.

- You need to close quickly.

- The interest rate advantage is relatively small.

- Another financing option better fits your financial goals.

Sometimes a traditional VA loan or even a conventional loan may actually be the simpler and more practical solution.

Every buyer’s situation is different.

Should You Search Specifically for Assumable Loans?

This is one of the questions I hear most often.

My answer is:

Yes, if an assumable loan fits your financial goals. But it helps to have a plan before we start looking.

One of the first things I ask buyers is how much they’ve set aside for the gap amount and closing costs. Having that conversation early helps us determine which assumable loans may realistically be within reach.

Once I understand your budget, I can keep an eye out for homes being marketed with VA assumable loans and do some of the legwork for you. That may include researching the remaining loan balance, estimating the potential gap amount, and determining whether the opportunity appears to fit your financial goals before we spend time pursuing it.

Not every listing advertised as “assumable” is automatically a good fit for every buyer. Some homes may have a very small gap amount, while others could require a significant amount of cash at closing.

That’s why I encourage buyers to think about the complete picture:

- Is the gap amount manageable?

- Does the assumption timeline work with your schedule?

- Is the monthly payment still affordable?

- Is this the right neighborhood?

- Does the home fit your lifestyle and long-term goals?

Sometimes an assumable loan is clearly the best option.

Other times, a traditional VA loan or another financing option may put you in a stronger position.

The goal isn’t simply to find an assumable loan. It’s to find the right home with financing that supports your overall goals.

A Low Interest Rate Doesn’t Automatically Mean It’s the Best Deal

One of the biggest misconceptions about VA assumptions is that every assumable loan is automatically a great deal simply because of the interest rate.

That’s not always the case.

A home with a 2.25% assumable loan may also require a buyer to bring a significant amount of cash to cover the seller’s equity.

Another home financed with a new VA loan may have a higher interest rate, but a lower purchase price, fewer upfront costs, or a financing structure that better fits the buyer’s financial goals.

That’s why I encourage buyers to compare the complete picture rather than focusing on a single number.

- The interest rate is important.

- The monthly payment is important.

- The amount of cash needed at closing is important.

- The home’s location is important.

- The home’s condition is important.

- Your long-term plans are important.

The best decision comes from looking at all of those pieces together.

Questions to Ask Before Pursuing a VA Assumption

If you’re considering an assumable loan, here are a few important questions to ask:

- What is the current interest rate?

- What is the remaining loan balance?

- How much equity does the seller have?

- Approximately how much cash will I need to bring to closing?

- Is the seller’s VA entitlement tied to this loan?

- How long is the assumption process expected to take?

- Has the mortgage servicer handled assumptions recently?

Having answers to these questions early can help you determine whether the opportunity is truly a good fit.

The Bottom Line

A VA assumable loan can be an incredible opportunity. A lower interest rate, fewer years remaining on the mortgage, and faster equity building can make assuming a loan an excellent option for some buyers.

At the same time, it isn’t the right solution for everyone. The seller’s equity, your available cash, your timeline, and your long-term goals all play an important role in determining whether assuming a loan makes financial sense.

My goal is to help buyers look beyond the advertised interest rate and evaluate the entire opportunity – from the gap amount and assumption timeline to the home’s location, condition, and long-term value.

The best financing option isn’t always the one with the lowest interest rate – it’s the one that helps you accomplish your goals with confidence.

If you’re planning a move to the San Antonio area and wondering whether a VA assumable loan makes sense for your situation, I’d be happy to walk through the numbers with you, compare your financing options, and help you determine the best path forward.

Jennifer Anderson is a San Antonio Realtor and military spouse who focuses on educating VA buyers and military families about using VA loans successfully – particularly in far west San Antonio neighborhoods. She combines local market knowledge with clear, practical guidance to help VA buyers make confident decisions.

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).